Last Updated on: Feb 11, 2024

By the fourth quarter of 2020, credit card debt reached $820 billion. Though the total amount of debt fell from the previous seven years, it has increasingly become more challenging for consumers to pay more than the minimum monthly payment.

What We'll Cover

For example, it would take a household more than 25 years to pay off credit card debt by only paying the monthly payment of $20 or 2% of the balance. With an interest rate of 12.4% (much lower than most credit card companies charge), the household would pay more than $9,800 in interest before paying the balance to zero dollars.

Though it may feel like there is no end to paying off credit card debt, government credit card debt relief programs are available. Several organizations can help reorganize, consolidate, reduce, and pay off credit card debt. The various government help programs for credit card debt can help consumers get out of debt faster while paying less interest and fees.

If you feel like you are drowning in debt and feel like there is no way out of your situation, continue reading to learn more about the various government help programs for credit card debt:

Are There Government Help Programs for Credit Card Debt?

The U.S. government offers programs assisting consumers in managing and eliminating various types of debt. However, as of {{current_year}}, no federal government-funded or government-sponsored programs provide consumers with relief from credit card debt. Unlike student loans, people with credit card debt cannot file with any government programs to have the debt reduced or forgiven.

What Can I Do if There Are No Government Help Programs for Credit Card Debt?

Though there are no official government-backed programs to help eliminate credit card debt, there are many things consumers can do. The Federal Trade Commission offers various options, tips, and information to help people with unmanageable credit card debt.

Credit card debt relief and management may include credit counseling, consolidation, budget management, and bankruptcy.

Are There Programs to Help With Credit Card Debt?

Several programs offer consumers help with credit card debt, providing customized and personalized solutions to meet their budget and debt needs. You can work with a Debt Relief company, or you can also obtain a personal loan to consolidate all of your credit card debt into a personal loan with a lower interest and a lower overall payment. Continue reading to learn more about some of the top credit card debt relief and personal loan companies available:

Credit Associates

CreditAssociates.org is our top pick for debt consolidation. Their services have seamlessly addressed the diverse financial challenges of thousands of clients, including credit cards, medical bills, student loans, taxes, utility bills, collection bills, and even payday loans.

What sets CreditAssociates.org apart is their commitment to personalized solutions. The team worked tirelessly to consolidate their clients' debts into a manageable monthly payment, significantly reducing the stress associated with multiple creditors. Their adept negotiation skills resulted in more favorable terms, lower interest rates, and even reduced overall debt amounts.

Transparency and trust are evident in every interaction, with CreditAssociates.org keeping me informed throughout the process. The educational resources provided helped their customers better understand their financial situation, empowering them to make informed decisions about their debt.

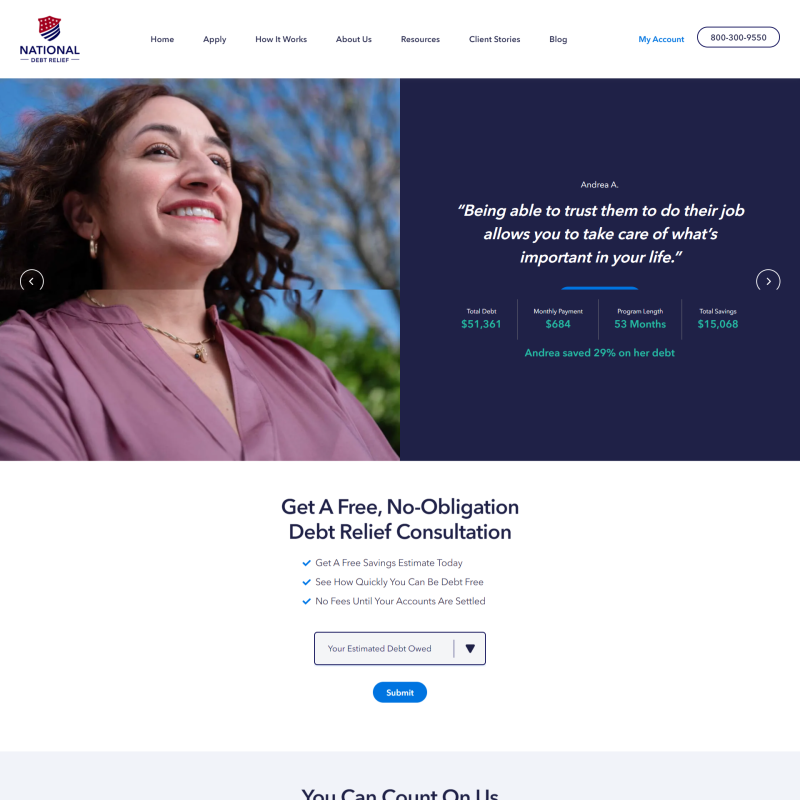

National Debt Relief

Since 2009, National Debt Relief has assisted hundreds of thousands of people in eliminating credit card debt. Working with this organization, you can save over 25 percent of your total debt, consolidating everything into lower, more affordable monthly payments. To qualify for help from National Debt Relief, you must have at least $10,000 in total debt, making this the best option for those with more significant debt.

LendingClub.com

Using LendingClub.com for debt consolidation can offer several benefits for individuals looking to manage their debt more effectively. Here are some of the advantages:

- Lower Interest Rates: One of the primary benefits of using LendingClub for debt consolidation is the potential to secure a personal loan with a lower interest rate compared to credit cards or other high-interest loans. This can lead to significant savings over time.

- Simplified Repayment: Consolidating multiple debts into a single loan with LendingClub means you only have one monthly payment to manage, making it easier to keep track of your finances and reduce the risk of missed payments.

- Fixed Monthly Payments: LendingClub offers fixed-rate personal loans, which means your monthly payments remain consistent throughout the loan term. This predictability can help you budget more effectively.

- Reduced Debt Stress: Managing multiple debts can be stressful. Debt consolidation with LendingClub can alleviate that stress by streamlining your finances and reducing the number of creditors you need to deal with.

- Improved Credit Score: If you use a LendingClub loan to pay off high-interest credit card debt and maintain responsible payment behavior, your credit score may improve over time. Lowering your credit utilization ratio and making on-time payments can positively impact your credit profile.

- Flexible Loan Terms: LendingClub offers a range of loan terms, allowing you to choose a repayment plan that best suits your financial goals and circumstances.

- Transparency: LendingClub is known for its transparent fee structure. You can easily see the interest rate, origination fees, and other costs associated with your loan before you commit.

- Online Convenience: LendingClub's online platform makes it convenient to apply for a loan, manage your account, and monitor your progress towards debt repayment.

- No Prepayment Penalties: LendingClub loans typically do not have prepayment penalties, so you can pay off your debt consolidation loan early without incurring additional fees.

- Potential for Debt Payoff: By consolidating your debts, you can create a clear path toward becoming debt-free. This can be a motivating factor in your financial journey.

It's important to note that while LendingClub can be a useful tool for debt consolidation, its effectiveness depends on your individual financial situation, creditworthiness, and responsible financial management. Before consolidating debt, carefully assess the terms and costs associated with the loan to ensure it aligns with your goals and budget. Additionally, make a commitment to avoid accumulating new debt while repaying the consolidation loan to achieve long-term financial stability.

LendingTree.com

LendingTree.com offers a valuable avenue for individuals looking to reduce their credit card debt burden. Users can take advantage of this platform by creating an account and submitting a loan request form, specifying their intention to tackle credit card debt. LendingTree then matches users with a selection of lenders who specialize in debt consolidation loans, balance transfer credit cards, or other financial products suitable for credit card debt reduction.

Through LendingTree, borrowers gain the ability to compare multiple offers from different lenders, considering factors such as interest rates, loan terms, and repayment options. Once a suitable lender is chosen, borrowers can proceed to complete the formal application process, which typically involves a credit check and document submission. Upon approval, borrowers can use the funds obtained to pay off their credit card balances, effectively consolidating their credit card debt into a more manageable and potentially lower-interest loan or credit card.

LendingTree.com facilitates a simplified approach to tackling credit card debt, potentially leading to reduced interest costs and a clearer path to financial freedom. However, individuals should exercise responsible financial management to avoid falling back into credit card debt.

How Do I Choose a Credit Card Debt Relief Company to Work With?

Before working with a credit card debt relief company, you must ensure you have exhausted all other financial options. Some people work with a non-profit credit counseling service as an alternative to determine if it is possible to reduce and eliminate debt on their own without having to pay fees to relief companies.

Additionally, every company is different, offering different programs, fees, requirements, and services. Do some research and schedule consultations with each company you are interested in to help better determine if the company is the best fit for your credit card debt relief needs.

According to the Consumer Financial Protection Bureau, speaking with your state Attorney General or local consumer protection agencies is also recommended to check for any consumer complaints about the debt relief company. Additionally, verify the company you want to work with is licensed to conduct business in your state.

What Should I Be Aware of Before Working With a Debt Relief Company?

It would be best to look for several things when deciding on a debt relief company to help manage, reduce, and eliminate your debt. Some things to beware of include:

- Paying fees upfront

- Guarantees on debt settlement

- I suggest you stop communicating with creditors

How Can I Manage Credit Card Debt Myself?

Working with a debt relief company to eliminate credit card debt can be helpful, especially when dealing with creditors. However, it is possible to manage, settle, and pay off your debt independently if desired. Working on debt management and relief yourself may take longer than when working with a company, but it can help you see more of the negative impact having large amounts of credit card debt can have on your finances.

Some things you can do to manage your credit card debt on your own may include the following:

- Call and speak with your creditors to discuss your options and if there is a possibility to settle the debt. It may be possible to reduce your interest rate, which can help reduce the total amount owed.

- Pay all bills on time to eliminate added late fees and other charges to your balance.

- Develop a realistic budget for all your bills and stick to it.

- Reduce spending and put all extra money toward paying off credit card debt.

- Choose a credit card payment strategy (see below).

- Stop using credit cards for purchases.

Credit Card Payment Strategies

Several financial strategies can help you pay off your credit card debt, and the one you choose must fit your budget and financial situation. Typical credit card payment strategies may include:

- Snowball payments: Pay the card with the lowest balance first, then move on to the next until all credit card debt is paid in full.

- Avalanche payments: Pay the card with the highest interest rate first and work down from there.

- Automating payments: Setting auto payments for your credit cards higher than the minimum due.

- Cut back on expenses: Cutting back on all expenses and putting that money toward credit cards can help pay off the debt faster.

- Consolidate or transfer debt: Rolling all of your high-interest credit card debt into one lower-interest account helps reduce the amount you’ll have to pay in interest while working on eliminating the debt.

FAQs About Credit Card Debt Relief

What Is Credit Card Debt Relief?

Credit card debt relief, also known as debt settlement, is a program and service that helps people reduce the amount of their high credit card debt. Working with a debt relief company means the company negotiates with your creditors to help lower the total amount you owe for all your unsecured debts, including credit card debt. Debt relief only typically works for secured credit cards if the amount you owe exceeds the deposit you made when you opened the account.

What Does a Credit Card Debt Relief Company Do?

A credit card debt relief company will negotiate the amount you owe a creditor, and the company pays for the agreed amount. Then, the company sets up a monthly payment plan often lower than all your monthly payments combined, making it easier to pay back the newly negotiated debt. Additionally, the company will add any of its fees and costs to what you owe them and include it in your monthly payments.

Be careful when working with a debt relief company because depending upon the amount of your debt and how much it can be settled for, with the debt relief company’s fees added on, you could end up paying more than if you slowly worked on paying off the debt on your own.

What Is the Difference Between Debt Consolidation and Debt Relief?

Though the goals of debt consolidation and debt relief are the same, there are significant differences between the two credit card debt management.

Debt consolidation relies on a personal loan to pay off all credit card debt, creating one payment versus multiple monthly payments. Consolidation can be done on your own, or there are credit card debt management companies that can help with consolidation.

Debt relief is a program where the debt is negotiated so the consumer pays less than they owe on their total credit card debt. A debt relief company can help negotiate with your creditors but will charge fees for their services.

How Much Does Debt Relief Cost?

Credit card debt relief companies charge a fee for their services, and the amount is based on the total amount you owe your creditors. On average, debt relief services cost 15 to 25 percent of the total debts when enrolled in the program. But remember that you may be paying less long-term as long as your debt is negotiated correctly and significantly reduced.

Will Debt Relief Destroy My Credit?

Though credit card debt relief can help reduce the damage to your credit history long-term, it does cause scores to drop. Many people who have gone through debt relief or debt settlement have experienced a 100-point decrease in their credit score. https://www.nfcc.org/

Can I Manage My Debt Relief on My Own?

Debt relief relies on settling credit card debt with creditors for less than the amount owed. Though you can do this independently, paying the debt can take time, patience, and upfront savings once a settlement is reached. Working with a debt relief company takes the stress of negotiating with creditors because they handle everything for you.

Would I Be Better off Filing for Bankruptcy?

The decision to file bankruptcy versus working on debt relief is personal and based on the individual’s financial situation. Filing for bankruptcy often requires an attorney and involves the courts to wipe out (Chapter 7) or reorganize (Chapter 13) your debt. Credit relief does not require the assistance of an attorney or the need to file anything with the courts.

Eliminating credit card debt is a crucial factor in securing your financial future. Excessive credit card debt may prevent you from doing many things, such as buying a home, getting an apartment, or buying a vehicle. Plus, excessive credit card debt can make it challenging to save for your future and buy the things you want and need.

Even though there are no government-operated programs, a credit card debt relief company can help you manage your current credit card debt and help you reduce and eliminate it. If you need help with credit card debt, seek the guidance and assistance of a debt relief company to learn more about the various programs available to you.

The responses below are not provided, commissioned, reviewed, approved, or otherwise endorsed by any financial entity or advertiser. It is not the advertiser’s responsibility to ensure all posts and/or questions are answered.